Have you ever looked at a job advert offering £15 or £20 per hour, quickly worked out your weekly earnings and then wondered why your payslip showed a much lower amount?

It’s a common experience. Your advertised hourly wage is usually your gross pay, the amount you earn before deductions. However, the money that actually reaches your bank account is your net pay, also known as your take-home pay. Income Tax, National Insurance contributions, pension deductions and other payroll adjustments can all reduce the amount you receive.

This is where an Hourly Wage Calculator After Tax UK becomes useful. Instead of relying on rough estimates, it helps you understand what you’ll actually take home based on your hourly rate, working hours, tax year and other payroll details.

Whether you’re starting a new job, comparing multiple job offers, working part-time or simply planning your monthly budget, knowing your after-tax hourly earnings gives you a clear picture of your finances.

In this guide, you’ll learn how an hourly wage calculator works, what affects your take-home pay, how to estimate your net hourly wage manually and why your actual payslip sometimes differs from the calculator’s estimate.

Calculator

What Is an Hourly Wage Calculator After Tax UK?

An Hourly Wage Calculator After Tax UK estimates how much of your hourly earnings you actually keep after mandatory payroll deductions have been applied.

Rather than showing only your gross hourly rate, the calculator estimates your:

- Net hourly pay

- Weekly take-home pay

- Monthly take-home pay

- Annual take-home salary

The calculation takes into account the UK’s payroll system, including Income Tax and National Insurance, while also considering optional deductions such as workplace pensions or student loan repayments.

For employees, agency workers, contractors paid through PAYE, and many part-time workers, it provides a far more realistic estimate than simply multiplying an hourly rate by the number of hours worked.

Definition and Purpose

The primary purpose of an hourly after-tax calculator is to answer one important question:

“How much money will actually reach my bank account after deductions?”

Instead of focusing only on advertised pay rates, the calculator estimates disposable income, making it easier to:

- Compare different job offers

- Plan monthly expenses

- Estimate annual income

- Budget for savings

- Understand the impact of tax changes

- Check whether a payslip looks reasonable

Although it provides an estimate rather than an official payroll calculation, it offers a reliable starting point for financial planning.

Gross Hourly Pay vs Net Hourly Pay

One of the biggest sources of confusion is the difference between gross pay and net pay.

| Gross Hourly Pay | Net Hourly Pay |

|---|---|

| Earnings before deductions | Earnings after deductions |

| Advertised by employers | Paid into your bank account |

| Does not include tax or National Insurance | Reflects actual take-home pay |

| Usually appears in job advertisements | Appears on your payslip |

For example:

If you’re offered £18 per hour, you won’t necessarily receive £18 for every hour worked. Depending on your income and personal circumstances, your take-home pay may be noticeably lower after deductions.

This distinction is why budgeting based solely on your gross wage can lead to inaccurate expectations.

Read More: Salary to Hourly Calculator UK – Easy Salary Converter 2026Why Your Take-Home Hourly Pay Is Lower Than Your Wage

Many first-time employees are surprised when they receive their first payslip.

Several deductions may reduce your gross earnings before payment is made.

Common deductions include:

- Income Tax

- National Insurance contributions (NIC)

- Workplace pension contributions

- Student loan repayments (where applicable)

- Salary sacrifice arrangements

- Other employer-specific deductions

Not everyone pays the same amount.

Two employees earning the same hourly wage could receive different net pay because they have different:

- Tax codes

- Pension contribution rates

- Student loan plans

- Working hours

- Bonus payments

- Salary sacrifice benefits

- Scottish or rest-of-UK tax rules

As a result, after-tax income is always personal to your circumstances

How Does an Hourly Wage Calculator After Tax UK Work?

An after-tax hourly wage calculator combines your pay details with current UK payroll rules to estimate your take-home earnings.

Instead of using a simple multiplication formula, it performs several calculations.

- Calculate your gross earnings.

- Apply the relevant Income Tax rules.

- Calculate National Insurance contributions.

- Deduct workplace pension contributions if applicable.

- Include student loan repayments where required.

- Estimate your final take-home pay.

- Convert the result into hourly, weekly, monthly and annual figures.

The result is a more realistic estimate of what you’ll actually receive.

Information You Need to Enter

Providing accurate information improves the accuracy of the estimate.

| Calculator Input | Description |

|---|---|

| Hourly Rate | Start by entering your agreed hourly wage before deductions. For example: • £12/hour • £15/hour • £18.50/hour • £25/hour |

| Hours Worked | Enter the number of paid hours you work. This could be: • Per week • Per month • Variable shift patterns • Part-time hours • Full-time hours. If your hours change regularly, consider using your average paid hours over several weeks for a more representative estimate. |

| Pay Frequency | Your pay schedule affects how payroll is processed. Common options include: • Weekly • Fortnightly • Four-weekly • Monthly • Annually Selecting the correct pay frequency helps the calculator apply deductions more accurately. |

| Tax Year | UK tax thresholds, allowances and rates can change from one tax year to the next. Always choose the correct tax year when using the calculator. Using outdated thresholds may lead to an inaccurate estimate of your take-home pay. |

| Pension Contributions | Many employees contribute to a workplace pension through automatic enrolment. Depending on your pension arrangement: • Contributions may reduce your taxable income. • They may reduce your take-home pay. The impact varies depending on how the pension is administered through payroll. Including your pension details provides a more realistic estimate. |

| Student Loan Repayments (Optional) | If you’re repaying a student loan through PAYE, repayments may be deducted automatically once your earnings exceed the applicable threshold for your repayment plan.Selecting the correct option helps the calculator estimate your net pay more accurately. |

How the Calculator Estimates Your Net Pay

Although different calculators use slightly different methods, most follow the same overall process:

- Calculate gross earnings from your hourly rate and working hours.

- Apply the relevant Income Tax rules.

- Calculate National Insurance contributions.

- Deduct pension contributions where applicable.

- Include student loan repayments if selected.

- Estimate your final take-home pay.

- Display results across multiple pay periods, including hourly, weekly, monthly and annually.

This allows you to see how your hourly wage translates into actual disposable income over time.

Formula Used to Calculate Take-Home Hourly Pay

At its simplest, the calculation follows this structure:

| Calculation | Formula |

|---|---|

| Gross Earnings | Gross Earnings = Hourly Rate × Hours Worked |

| Net Pay | Net Pay = Gross Earnings − Total Payroll Deductions |

| Net Hourly Pay | Net Hourly Pay = Net Pay ÷ Total Hours Worked |

While the formula appears straightforward, the deductions themselves depend on several variables, including tax bands, National Insurance thresholds, pension contributions, tax codes and other payroll adjustments. That’s why an after-tax calculator provides a more accurate estimate than manual calculations based on gross pay alone.

Understanding how the calculator works is only the first step. The next section explores the factors that influence your take-home pay, including Income Tax, National Insurance, pension contributions, student loans, salary sacrifice schemes, Scottish tax rates and overtime helping you understand why two people earning the same hourly rate can end up with different net pay.

What Affects Your Hourly Take-Home Pay in the UK?

Your hourly rate is only one part of the equation. The amount you actually receive depends on several payroll deductions and personal circumstances.

For example, two employees earning £18 per hour may take home different amounts because one contributes more to a workplace pension, while the other repays a student loan or has a different tax code.

Understanding these factors helps you interpret calculator results more accurately and explains why your payslip may not match someone else’s even if your hourly wages are identical.

Income Tax Bands

Income Tax is usually the largest deduction from your earnings.

The UK uses a progressive tax system, meaning different portions of your income are taxed at different rates rather than one single rate.

| Topic | Explanation |

|---|---|

| Personal Allowance | Generally, everyone may be entitled to a Personal Allowance, subject to eligibility. |

| Tax Bands | Earnings above the allowance are taxed in bands. |

| Higher Earnings | Higher earnings move into higher tax bands. |

| How UK Income Tax Works | A small pay rise doesn’t mean all of your income is taxed at the higher rate. Only the portion of income within a higher tax band is taxed at that higher percentage. |

Why It Matters

If your annual income increases because you:

- Work more hours

- Receive overtime

- Get a promotion

- Earn bonuses

Your estimated take-home hourly pay may change even if your basic hourly rate stays the same.

Important: Income Tax rates and thresholds can change between tax years. Always select the correct tax year when using an after-tax calculator.

National Insurance Contributions (NIC)

National Insurance Contributions (NICs) are separate from Income Tax.

Most employees pay NICs once their earnings exceed the applicable threshold.

These contributions help fund benefits such as:

- State Pension

- Maternity benefits

- Certain employment-related benefits

Unlike Income Tax, National Insurance has its own rules and thresholds.

Even if your Income Tax is relatively low, you may still pay National Insurance depending on your earnings.

Why NIC Matters

Many people estimate their pay by subtracting Income Tax alone.

However, National Insurance can make a noticeable difference to your take-home pay.

A good hourly wage calculator includes both deductions automatically.

Pension Contributions

Many UK employees are automatically enrolled in a workplace pension.

Although pension contributions reduce your immediate take-home pay, they help build retirement savings and may provide valuable employer contributions.

Depending on your employer’s pension arrangement:

- Contributions may be deducted before tax.

- Contributions may be deducted after tax.

- Employer contributions do not normally count as part of your take-home pay.

Example

Suppose two employees earn the same hourly rate.

| Employee | Pension Contribution | Immediate Take-Home Pay |

|---|---|---|

| Employee A | No pension | Higher |

| Employee B | Workplace pension | Slightly lower |

While Employee B receives less today, they are building retirement savings that may include additional employer contributions.

Student Loan Repayments

If you’re repaying a UK student loan through PAYE, repayments may begin once your earnings exceed the threshold for your repayment plan.

The amount deducted depends on factors such as:

- Your repayment plan

- Your earnings

- Payroll calculations

If you are below the repayment threshold, no deduction is normally made.

Including student loan information in the calculator helps produce a more realistic estimate of your net pay.

Salary Sacrifice Schemes

Some employers offer salary sacrifice arrangements.

Instead of receiving part of your salary as cash, you exchange it for specific benefits.

Common examples include:

- Additional pension contributions

- Cycle-to-work schemes

- Electric vehicle schemes

- Childcare-related benefits (where applicable)

Because salary sacrifice reduces your taxable salary, it can sometimes lower:

- Income Tax

- National Insurance contributions

This means your take-home pay may not decrease by the full amount sacrificed.

Scottish Income Tax vs England, Wales and Northern Ireland

One important factor many employees overlook is where they pay Income Tax.

Employees living in Scotland generally follow Scottish Income Tax rates and bands for non-savings, non-dividend income.

Employees in:

- England

- Wales

- Northern Ireland

generally follow the UK Income Tax bands that apply outside Scotland.

Why This Matters

Two employees earning the same hourly wage could receive different net pay simply because one is taxed under Scottish Income Tax rules while the other is not.

Most quality after-tax calculators allow you to select the correct tax jurisdiction before calculating your take-home pay.

Tax Code Changes

Your tax code tells your employer how much tax to deduct from your wages.

| Topic | Explanation |

|---|---|

| Effects of an Incorrect Tax Code | An incorrect tax code can result in: • Paying too much tax • Paying too little tax • Temporary payroll adjustments |

| Common Reasons Your Tax Code May Change | Common reasons your tax code may change include: • Starting a new job • Having more than one employer • Receiving taxable benefits • Changes to your Personal Allowance • Corrections made by HMRC |

If your calculator assumes a standard tax code but your actual code is different, your estimate may not exactly match your payslip.

Overtime, Bonuses and Shift Premiums

Extra earnings don’t always affect your pay in the same way as your standard hourly wage.

| Topic | Explanation |

|---|---|

| Additional Payments | Additional payments may include: • Overtime • Night shift premiums • Weekend enhancements • Performance bonuses • Commission |

| Impact on Your Pay | These payments increase your gross earnings and may also increase: • Income Tax • National Insurance • Student loan repayments |

As a result, the extra amount deposited into your bank account may be less than expected after deductions.

Using an after-tax calculator that includes overtime or bonus payments gives a much more accurate estimate than calculating your basic hourly wage alone.

Read More: gov.ukHow to Calculate Hourly Pay After Tax Manually

Although an online calculator is the quickest option, understanding the calculation process helps you verify estimates and better understand your payslip.

Here’s a simplified step-by-step method.

Step 1: Calculate Gross Earnings

Start with your hourly wage before deductions.

| Section | Details |

|---|---|

| Formula | Gross Earnings = Hourly Rate × Hours Worked |

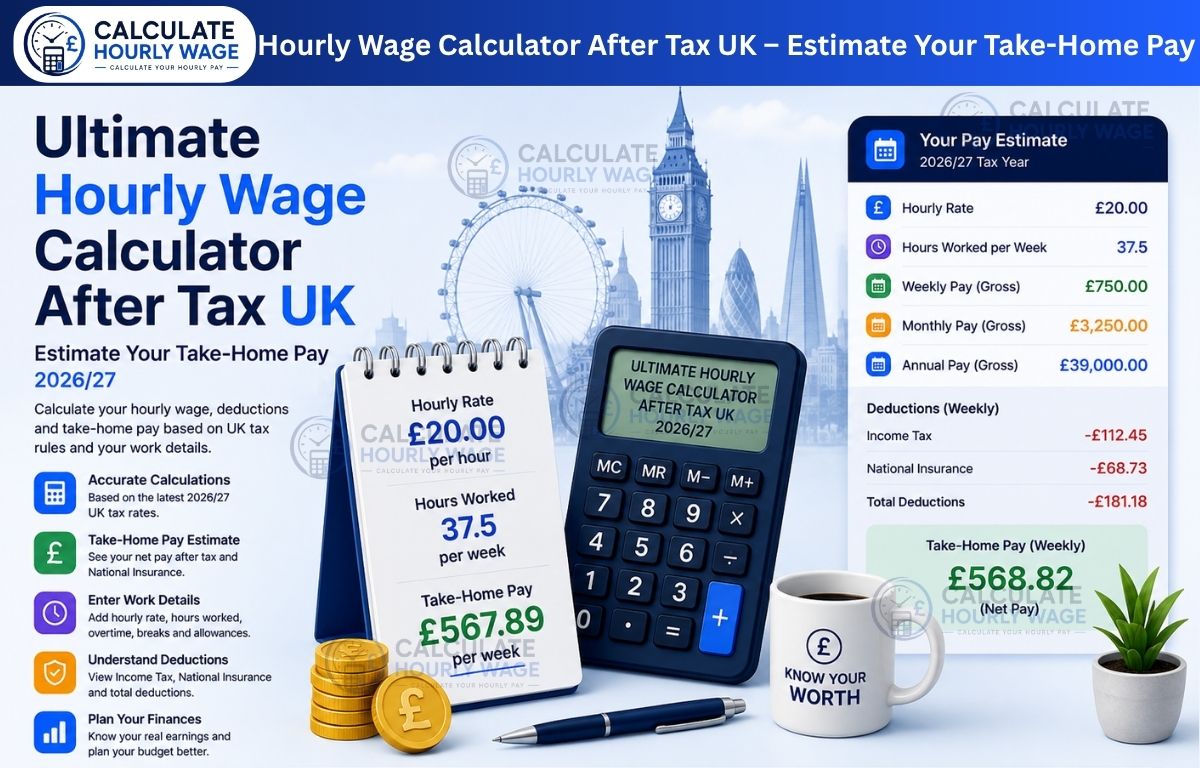

| Example | Hourly wage: £16 Hours worked: 37.5 per week Gross weekly earnings:£16 × 37.5 = £600 |

This is your gross pay before any deductions.

Step 2: Estimate Income Tax

Next, calculate any Income Tax due based on:

- Your annual earnings

- Personal Allowance (if applicable)

- Tax bands for the selected tax year

- Tax jurisdiction (Scotland or the rest of the UK)

Remember that tax is calculated on taxable income—not simply on every pound you earn.

Step 3: Calculate National Insurance

After Income Tax, estimate any National Insurance contributions based on:

- Your earnings

- Current NIC thresholds

- Employee contribution rules

National Insurance is calculated separately from Income Tax, so both deductions need to be considered.

Step 4: Subtract Other Payroll Deductions

Depending on your circumstances, additional deductions may include:

- Workplace pension

- Student loan repayments

- Salary sacrifice arrangements

- Other authorised payroll deductions

These reduce the amount that reaches your bank account.

Step 5: Find Your Net Hourly Wage

Once all deductions have been made, calculate your effective hourly take-home pay.

Formula

Net Hourly Wage = Net Pay ÷ Hours Worked

Example

Suppose your figures look like this:

| Item | Amount |

|---|---|

| Gross weekly pay | £600 |

| Income Tax | −£48 |

| National Insurance | −£29 |

| Pension contribution | −£18 |

| Net weekly pay | £505 |

Now divide your net pay by the hours worked:

£505 ÷ 37.5 = £13.47 per hour (approximately)

Although your employer pays £16 per hour, your estimated take-home pay is about £13.47 per hour after deductions.

This illustrates why using an Hourly Wage Calculator After Tax UK provides a far more realistic picture of your earnings than looking at your gross hourly rate alone.

Hourly Wage After Tax Examples

The examples below illustrate how different hourly rates can translate into take-home pay. These are illustrative estimates, not exact payroll calculations.

Your actual net pay will depend on factors such as:

- Your tax code

- The tax year selected

- National Insurance thresholds

- Pension contributions

- Student loan repayments

- Salary sacrifice arrangements

- Overtime or bonus payments

- Whether you’re taxed under Scottish or rest-of-UK Income Tax rules

Use these examples to understand the relationship between gross hourly pay and estimated take-home pay, rather than as guaranteed figures.

Read More: National Insurance Calculator UK – Ultimate Guide to NI Contributions 2026/27£12 Per Hour After Tax

An hourly rate of £12 is common in many entry-level and customer-facing roles.

If you work full-time, your annual earnings may exceed certain payroll thresholds, meaning deductions such as Income Tax and National Insurance could apply depending on the current tax year and your circumstances.

This hourly rate is often seen in:

- Retail

- Hospitality

- Warehousing

- Customer service

- Care work

If you work part-time, your deductions may be lower because your annual taxable income is also lower.

£15 Per Hour After Tax

At £15 per hour, gross earnings increase noticeably, but so can payroll deductions.

Many employees at this pay level are surprised that a pay rise doesn’t translate into the same increase in take-home pay.

That’s because additional earnings may increase:

- Income Tax

- National Insurance

- Student loan repayments (if applicable)

Even so, your overall disposable income still increases—you simply don’t keep every additional pound earned.

£20 Per Hour After Tax

Earning £20 per hour can provide a comfortable income for many full-time workers.

At this level, accurate payroll calculations become more important because deductions usually have a greater impact than they do at lower hourly rates.

Employees often use an after-tax calculator when:

- Comparing job offers

- Negotiating salary

- Budgeting for rent or mortgages

- Estimating annual take-home pay

£25 Per Hour After Tax

A rate of £25 per hour is common in many skilled professions and technical roles.

Examples include:

- IT professionals

- Engineers

- Experienced tradespeople

- Consultants

- Healthcare specialists

As earnings increase, understanding tax efficiency becomes more valuable.

Many employees at this level review:

- Pension contribution levels

- Salary sacrifice options

- Tax codes

- Workplace benefits

These factors can influence overall take-home pay.

£30 Per Hour After Tax

An hourly wage of £30 often represents experienced professionals, contractors working through PAYE, or specialist employees.

Although gross earnings are significantly higher, payroll deductions are also likely to increase.

This makes accurate after-tax calculations essential when:

- Accepting a new contract

- Switching employers

- Planning annual income

- Estimating monthly disposable income

Full-Time vs Part-Time Examples

Your hourly rate isn’t the only factor that determines your take-home pay.

Working more hours increases your gross income, but it can also increase payroll deductions.

For example:

| Working Pattern | Hours per Week | Gross Weekly Earnings (at £15/hour) |

|---|---|---|

| Part-time | 20 | £300 |

| Part-time | 25 | £375 |

| Full-time | 37.5 | £562.50 |

| Full-time | 40 | £600 |

Although the hourly rate stays the same, total annual earnings—and therefore payroll deductions—change with the number of hours worked.

Hourly Wage After Tax Comparison Tables

Comparison tables make it easier to estimate how different hourly rates translate into longer pay periods.

Remember that these figures represent gross earnings before deductions. Your actual take-home pay will vary based on your personal tax situation.

Estimated Gross Earnings by Hourly Rate

| Hourly Rate | Weekly (37.5 hrs) | Monthly* | Annual* |

|---|---|---|---|

| £12 | £450 | £1,950 | £23,400 |

| £15 | £562.50 | £2,437.50 | £29,250 |

| £20 | £750 | £3,250 | £39,000 |

| £25 | £937.50 | £4,062.50 | £48,750 |

| £30 | £1,125 | £4,875 | £58,500 |

Approximate values based on a consistent 37.5-hour working week.

Estimated Take-Home Pay Overview

After deductions, your actual pay will usually be lower than the gross figures above.

A calculator considers factors including:

| Deduction | Included in Calculator |

|---|---|

| Income Tax | ✔ |

| National Insurance | ✔ |

| Pension Contributions | ✔ (where entered) |

| Student Loan | ✔ (optional) |

| Salary Sacrifice | ✔ (where applicable) |

| Tax Code | ✔ (where supported) |

This provides a much more realistic estimate than relying solely on gross earnings.

Comparison Across Different Weekly Hours

The same hourly rate produces different annual earnings depending on the number of hours worked.

Using £18 per hour as an example:

| Hours per Week | Weekly Gross | Approximate Annual Gross |

|---|---|---|

| 16 | £288 | £14,976 |

| 20 | £360 | £18,720 |

| 25 | £450 | £23,400 |

| 30 | £540 | £28,080 |

| 37.5 | £675 | £35,100 |

| 40 | £720 | £37,440 |

This comparison is particularly useful for:

- Part-time workers

- Students

- Agency workers

- Shift workers

- Employees considering overtime

Why Your Actual Payslip May Differ From the Calculator

Even the most accurate calculator provides an estimate.

Your employer’s payroll system calculates your actual pay using your specific employment details, which may include adjustments not entered into the calculator.

Here are some of the most common reasons for differences.

Emergency Tax Codes

If you’ve recently started a new job or your employer doesn’t yet have your correct tax information, an emergency tax code may be applied.

This can temporarily result in:

- Higher tax deductions

- Lower take-home pay

- Future tax refunds or adjustments once the correct code is applied

Bonuses and Overtime

Extra earnings during a pay period can increase:

- Taxable income

- National Insurance

- Student loan repayments

As a result, your net pay for that period may differ from a standard calculator estimate based only on your regular hourly wage.

Pension Arrangement Differences

Not all workplace pension schemes operate in the same way.

Your employer may use:

- Salary sacrifice

- Net pay arrangements

- Relief at source

Each method affects deductions differently, which can change your final take-home pay.

Student Loan Thresholds

If your earnings exceed your repayment threshold during a particular pay period, student loan deductions may begin or increase.

If the calculator doesn’t include the correct repayment plan, the estimate may differ from your payslip.

Benefits in Kind

Some employees receive taxable benefits such as:

- Company cars

- Private medical insurance

- Employer-paid expenses

These benefits can affect taxable income even though they are not paid as cash wages.

Employer Payroll Timing and Adjustments

Payroll may include adjustments such as:

- Back pay

- Holiday pay

- Sick pay

- Statutory payments

- Payroll corrections

- Salary arrears

These one-off adjustments can make your payslip differ from a standard after-tax estimate.

By understanding these variables, you can use an Hourly Wage Calculator After Tax UK more effectively as a planning tool rather than a replica of your payslip. In the final part, we’ll cover common mistakes, practical tips to maximise your take-home pay legally, related UK pay calculators and answer the most frequently asked questions.

Common Mistakes When Estimating Hourly Take-Home Pay

Even with an online calculator, small mistakes can lead to inaccurate estimates. Avoiding these common errors will help you get results that are much closer to your actual payslip.

| Common Mistake | Explanation |

|---|---|

| Confusing Gross Pay With Net Pay | This is the most common mistake. Gross pay is your earnings before deductions.Net pay (take-home pay) is the amount paid into your bank account after Income Tax, National Insurance, and other deductions. Always make sure you know which figure you’re looking at when comparing job offers or planning your budget. |

| Using the Wrong Tax Year | Income Tax bands, National Insurance thresholds, and other payroll rules can change from one tax year to the next. If you use an outdated tax year, your estimate may no longer reflect current payroll calculations. Best practice: Always select the current tax year before calculating your take-home pay. |

| Ignoring National Insurance | Some people only subtract Income Tax when estimating their earnings. However, National Insurance Contributions (NICs) are a separate deduction and can significantly affect your take-home pay. A reliable calculator includes both Income Tax and NIC automatically. |

| Forgetting Pension Contributions | If you’re enrolled in a workplace pension, your contributions reduce your take-home pay.Ignoring pension deductions can make your estimate appear higher than the amount you actually receive. |

| Assuming Everyone Has the Same Tax Code | Your tax code affects how much Income Tax your employer deducts.Using a standard tax code when your own tax code is different can lead to inaccurate estimates.If you’ve recently changed jobs or received a tax code notice, make sure you use the correct tax code when estimating your take-home pay. |

Tips to Increase Your Take-Home Pay Legally

While you can’t avoid mandatory taxes, there are legitimate ways to make sure you’re not paying more than necessary.

| Tip | Explanation |

|---|---|

| Check Your Tax Code Regularly | An incorrect tax code can result in overpaying Income Tax. Review your tax code periodically if you’ve: • Started a new job • Changed employers • Began a second job • Returned to work after a break • Received taxable benefits. Correcting an error early can prevent unnecessary deductions. |

| Review Pension Contribution Options | A workplace pension is a valuable long-term benefit, but it’s still worth understanding how your contributions affect your take-home pay. Review: • Your contribution percentage • Employer matching contributions • The type of pension arrangement used This helps you balance current income with future retirement savings. |

| Understand Salary Sacrifice Benefits | If your employer offers salary sacrifice, it may reduce your taxable salary while providing additional benefits. Common examples include: • Pension contributions • Cycle-to-work schemes • Electric vehicle schemes Depending on the arrangement, salary sacrifice may reduce both Income Tax and National Insurance. |

| Claim Any Tax Relief You’re Entitled To | Some employees are eligible to claim tax relief for certain work-related expenses, such as: • Professional membership fees • Uniform maintenance (where applicable) • Business mileage not reimbursed by an employer. Claiming eligible relief can reduce your overall tax liability. |

| Stay Up to Date With Tax Changes | Payroll rules don’t stay the same forever. Changes to: • Income Tax thresholds • National Insurance rules • Student loan repayment thresholds • Pension regulations can all affect your future take-home pay. Checking the latest rules each tax year helps ensure your estimates remain accurate. |

Related UK Pay Calculators You May Find Useful

An hourly after-tax calculator is only one of several useful payroll tools. Depending on your needs, you may also find these calculators helpful:

| Calculator | What It Helps You Do |

|---|---|

| Salary to Hourly Calculator UK | Convert an annual salary into an hourly rate. |

| Hourly to Salary Calculator UK | Estimate annual earnings from an hourly wage. |

| Income Tax Calculator UK | Calculate estimated Income Tax based on your income. |

| National Insurance Calculator UK | Estimate your NIC deductions. |

| Overtime Pay Calculator UK | Work out additional earnings from overtime hours. |

| Pro Rata Salary Calculator UK | Calculate pay for part-time or reduced working hours. |

Using these tools together can give you a more complete picture of your earnings throughout the year.

How do I calculate my hourly wage after tax in the UK?

Start by calculating your gross earnings from your hourly rate and hours worked. Then subtract Income Tax, National Insurance, pension contributions, and any other applicable payroll deductions. An Hourly Wage Calculator After Tax UK automates this process and provides a quicker estimate.

How much tax is deducted from my hourly pay?

There isn’t a fixed amount deducted from every hourly wage. The amount depends on your annual earnings, tax code, National Insurance, pension contributions, student loan repayments, and the tax year.

Does the calculator include National Insurance?

Yes. A good after-tax calculator estimates both Income Tax and National Insurance Contributions, giving a more realistic estimate of your take-home pay.

Can I calculate hourly take-home pay for part-time work?

Yes. Simply enter your hourly rate and the number of hours you normally work. The calculator estimates your take-home pay based on your working pattern and payroll information.

Why is my payslip different from the calculator estimate?

Your payslip may differ because of factors such as your tax code, bonuses, overtime, pension arrangements, student loan repayments, salary sacrifice, payroll adjustments, or taxable benefits.

Does a pension contribution reduce my take-home hourly wage?

Yes. Workplace pension contributions generally reduce your immediate take-home pay. However, they also help build your retirement savings and may include valuable employer contributions.

Can I calculate hourly pay after tax with overtime included?

Yes. If the calculator allows you to enter overtime or additional earnings, it can estimate how those extra payments affect your net pay after deductions.

Does the calculator work for Scotland as well as the rest of the UK?

Most modern UK payroll calculators allow you to select whether Scottish Income Tax rules apply. Choosing the correct option helps improve the accuracy of your estimate.

Which tax year should I choose when estimating my take-home pay?

Always select the tax year that matches the period you’re estimating. Using an outdated tax year can result in inaccurate calculations because tax thresholds and payroll rules may have changed.

Can I convert my annual salary into an hourly after-tax wage?

Yes. First convert your annual salary into an hourly rate based on your working hours, then apply Income Tax, National Insurance, and any other payroll deductions. Many salary calculators can perform both calculations automatically.

Conclusion

Understanding your advertised hourly wage is only part of the picture. What really matters is how much of that money you actually keep after Income Tax, National Insurance, pension contributions, and other payroll deductions. An Hourly Wage Calculator After Tax UK helps bridge that gap by providing a realistic estimate of your take-home pay, making it easier to budget, compare job offers, and plan your finances with confidence.

While no calculator can perfectly replicate every payslip, using accurate information such as the correct tax year, working hours, tax code, and payroll deductions will produce a reliable estimate for most employees. Use the calculator alongside this guide to better understand your earnings and make more informed financial decisions throughout the year.